On this page...

If you're retiring in the next few years, this video walks through how your IPERS benefit is calculated.

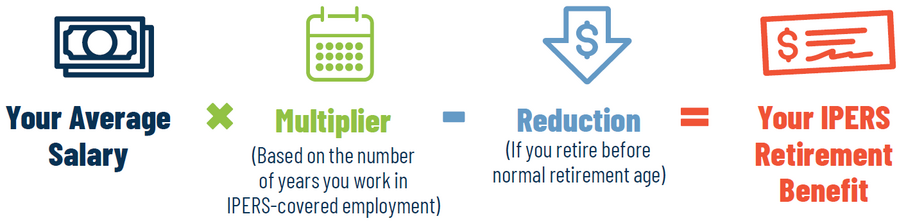

Your IPERS retirement benefit is calculated using three factors: your average salary, a multiplier based on your years of service, and a reduction if you retire before normal retirement age.

Log in to My Account to estimate your approximate payments.

Back to top

Average salary

This is the average of your highest five years' salaries. These don't have to be the five consecutive years immediately before retirement.

Wage spiking

Applies only if your salary increased significantly in your final years of employment. When calculating your benefit, IPERS tests for wage spiking, to prevent overpaying your benefits. Your average salary will be decreased if wage spiking occurred.

- To test your highest three-year average salary, IPERS compares it to a control-year salary (your highest calendar year salary outside of the three years in your average). If your highest three-year average exceeds 121% of your control-year salary, your salary in the formula will be reduced to 121% of your control-year salary.

- To test your highest five-year average salary, IPERS compares it to a control-year salary (your highest calendar year salary outside of the five years in your average). If your highest five-year average exceeds 134% of your control-year salary, your salary in the formula will be reduced to 134% of your control-year salary.

If you stop working before the end of a calendar year, IPERS will calculate your wages as follows:

- Look at your wages earned each quarter of your last year of employment

- Find your highest calendar year wage not used in the average salary calculation and calculate the average quarterly wage for that year

- Use that quarterly average for quarters you didn't work in your last year — this is your computed-year wage

If the computed-year wage is higher than your third- or fifth-highest calendar year wage, IPERS uses the computed-year wage as your final year's wage. The computed-year wage is limited to 103% of your highest calendar year wage and does not result in additional service credit.

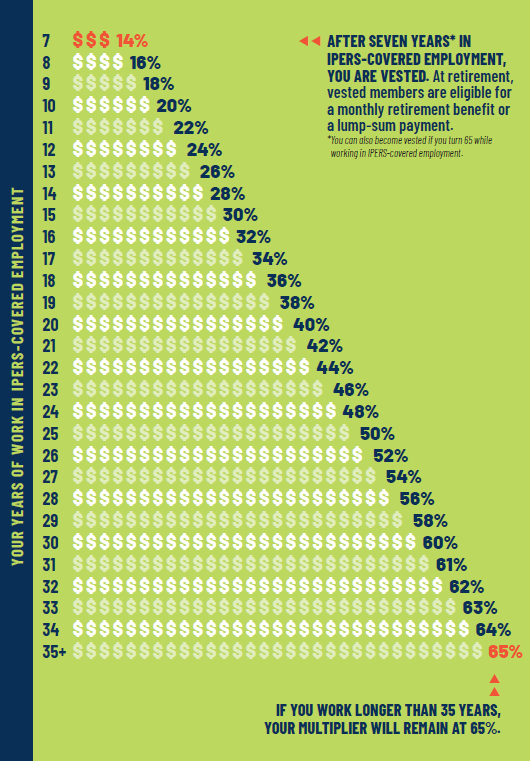

Back to topMultiplier

Your multiplier increases two percentage points for each year you work in IPERS-covered employment, up to year 30. From years 31–35, it increases one percentage point per year. The maximum multiplier is 65% at 35 years of service.

You may also purchase service at retirement to increase your multiplier.

Back to topReduction

A reduction applies if you retire before normal retirement age. Your benefit will be reduced by 0.5% for each month (6% annually) that you receive benefits before age 65.

Back to topHow it all fits together

Your benefit formula:

Average salary x multiplier - reduction (if any) = annual retirement benefit