If you're retiring in the next few years, this video walks through how your IPERS benefit is calculated.

Your IPERS retirement benefit is calculated using two factors: your average salary and a multiplier based on your years of service.

Log in to My Account to create estimates of your approximate payments.

Average salary

Your average salary is the average of your highest three years' IPERS-covered wages (January 1–December 31 each year). These don't have to be the three years immediately before retirement.

Wage spiking

Applies only if your salary increased significantly in your final years of employment. When calculating your benefit, IPERS tests for wage spiking to prevent overpaying benefits. Your average salary will be decreased if wage spiking occurred.

To test your highest three-year average salary, IPERS compares it to a control-year salary (your highest calendar year salary outside of the three years in your average). If your highest three-year average exceeds 121% of your control-year salary, your salary in the formula will be reduced to 121% of your control-year salary. Additional rules apply when your fourth-highest salary does not represent a full year of salary.

If you stop working before the end of a calendar year, IPERS will calculate your wages as follows:

- Look at your wages earned each quarter of your last year of employment

- Find your highest calendar year wage not used in the average salary calculation and calculate the average quarterly wage for that year

- Use that quarterly average for quarters you didn't work in your last year — this is your computed-year wage

If the computed-year wage is higher than your third-highest calendar year wage, IPERS uses the computed-year wage as your final year's wage. The computed-year wage is limited to 103% of your highest calendar year wage and does not result in additional service credit.

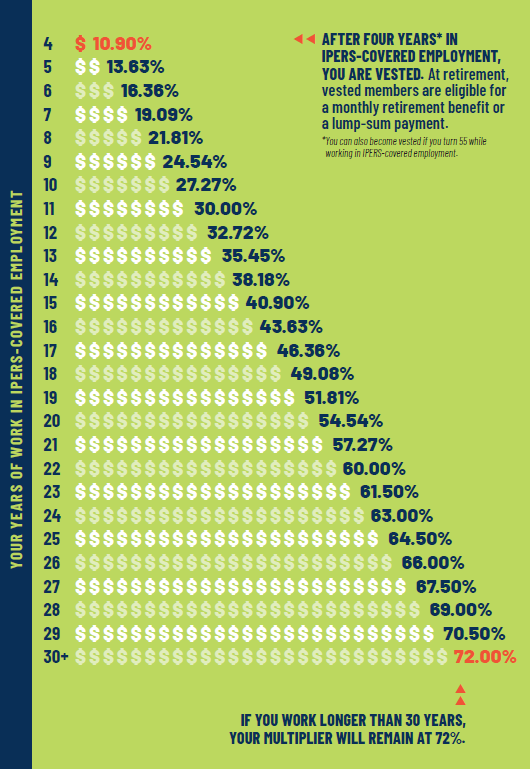

Multiplier

The multiplier increases each year you work in IPERS-covered employment. For Protection Occupations members, the multiplier increases approximately 2.7272% a year for the first 22 years of IPERS-covered work and 1.5% a year for years 23-30. The maximum multiplier is 72%. If you work longer than 30 years, the multiplier remains at 72%.

At retirement, you may purchase service at retirement to increase your multiplier.

Early retirement

If all your IPERS-covered jobs are Special Service positions, your benefit is not reduced for early retirement. If you worked in a Regular IPERS-covered position at any point in your career, a hybrid formula may be used to calculate your benefit, and a reduction may apply.

How it all fits together

Your benefit formula:

Average salary × multiplier = annual retirement benefit